Why Aren’t Loan Rates Dropping? The Bond Market’s Standoff with the Fed

Published on: December 10, 2025 | By: The Team at Mine Mirth LLC

Have you noticed that even though the Federal Reserve (the Fed) has been cutting interest rates, mortgage and loan rates aren’t really budging? You’re not imagining it. There’s a major, unusual tug-of-war happening right now between the Fed’s policy and the bond market, and it affects everyone’s wallet.

Normally, when the Fed lowers its key rate, borrowing costs across the economy follow suit. But this time, the bond market isn’t playing along. This split is so rare we haven’t seen anything like it since the 1990s.

Let’s break down what’s happening, why experts are debating fiercely, and what it could mean for you.

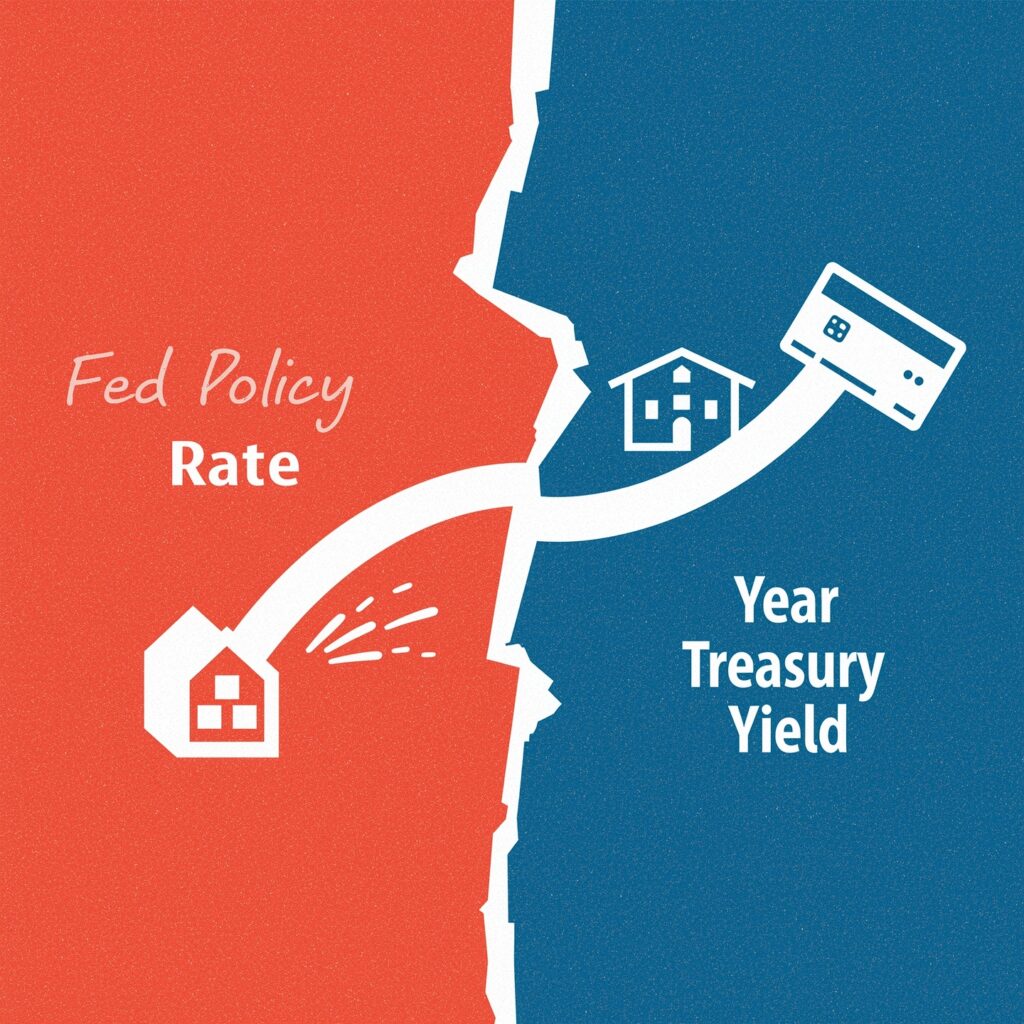

The Unusual Split: Fed Cuts vs. Rising Yields

In September 2024, the Fed began lowering its benchmark interest rate from a two-decade high to combat economic slowing. Since then, it has cut rates by 1.5 percentage points.

Yet, key Treasury bond yields—which directly influence mortgage rates, auto loans, and corporate borrowing—have risen. For example:

- The 10-year Treasury yield has climbed about 0.5%.

- The 30-year Treasury yield is up over 0.8%.

This disconnect defies the usual pattern. Even in past rare instances where the Fed cut rates without a recession (like in 1995 and 1998), long-term yields still fell. This time, they’re marching higher.

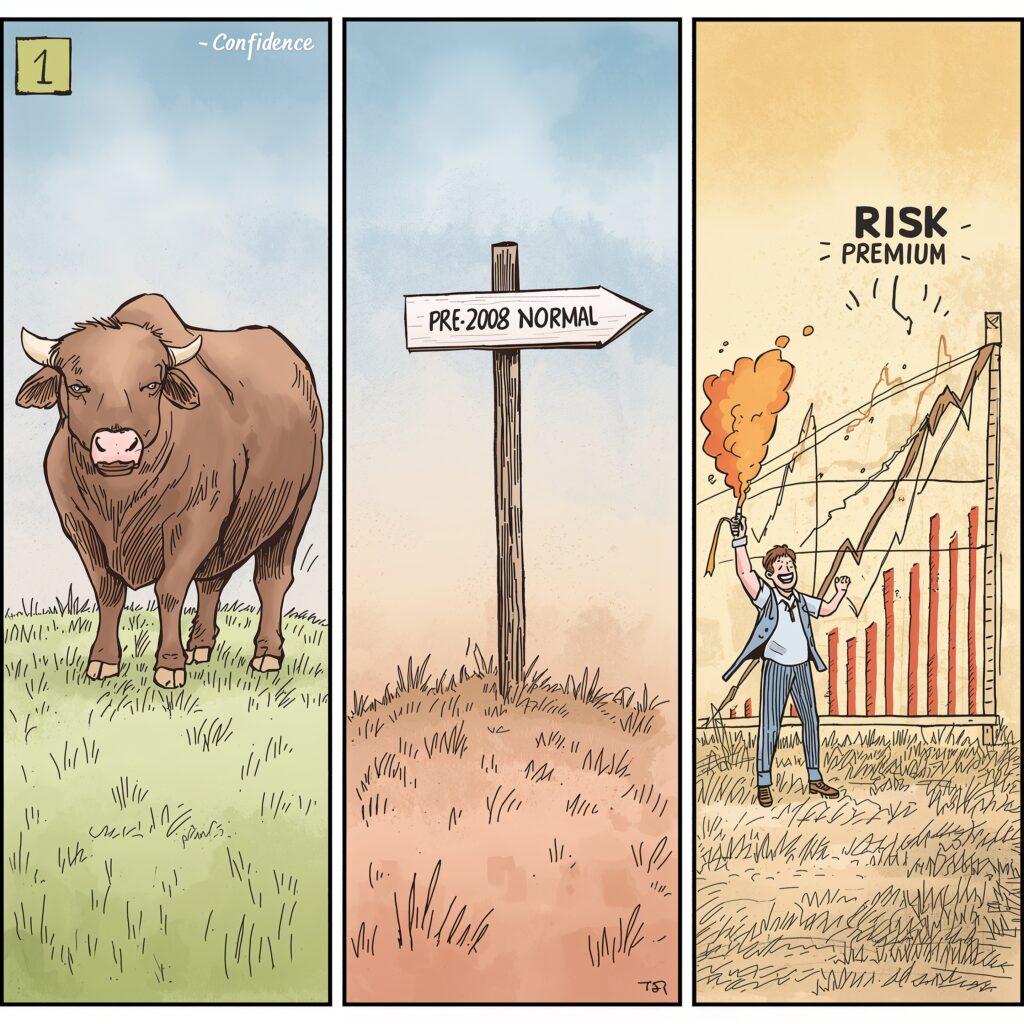

The Great Wall Street Debate: What’s Really Going On?

Why is the bond market defying the Fed? Analysts are divided into three main camps:

- The Bullish View (Confidence): This could signal a strong, “soft-landing” economy. The Fed is cutting rates preventatively to sustain growth, not in a panic. A robust economy can handle higher yields, so they don’t need to fall. As JPMorgan’s Jay Barry put it, “The Fed is looking to sustain this expansion, not end it.”

- The “New Normal” View (Back to Basics): We may simply be returning to the interest rate environment that existed before the 2008 financial crisis. The period of ultra-low rates from 2009-2021 was the historical anomaly. 4%+ yields might be the new (old) normal, as suggested by strategists like PGIM’s Robert Tipp.

- The Worried View (Bond Vigilantes): This camp believes investors are demanding higher yields as a risk premium. They are worried about two big issues: inflation remaining stubbornly above the Fed’s 2% target and concerns over the U.S. government’s growing national debt. Investors, in this view, need extra compensation for these long-term risks. (Bloomberg’s Ed Harrison explores this “normal regime” idea in depth).

The Political Wild Card

Former President Donald Trump has argued that faster rate cuts will bring down borrowing costs. However, many market veterans warn the opposite could happen.

The concern is that if the Fed is seen caving to political pressure to cut rates aggressively, it could backfire. It might damage the Fed’s hard-won credibility on fighting inflation, spook investors, and ironically push long-term yields even higher.

“Putting a political figure at the Fed will not get bond yields down,” warned Steven Barrow of Standard Bank.

What This Means for You

- Mortgage & Loan Rates: Don’t assume Fed rate cuts will automatically mean lower monthly payments on big loans. The bond market, which sets those rates, is telling a different story for now.

- The Fed’s Power Has Limits: This standoff highlights a crucial truth: while the Fed controls short-term policy, global market forces—driven by debt, inflation expectations, and global capital—ultimately determine long-term rates. As Barrow noted, “central banks don’t determine the long-term rate.”

- Stability for Now: It’s not all alarm bells. Broader market measures of inflation expectations have remained stable, suggesting a full-blown inflationary spiral isn’t imminent.

The Bottom Line from Mine Mirth

The bond market is sending a complex, critical message. Whether it’s signaling economic strength, a return to normalcy, or sounding a warning on fiscal policy, one outcome seems clear: the era of near-zero interest rates is firmly in the past.

For borrowers and investors, this means adjusting expectations and strategies for a world where the cost of money has a more normal, substantial price tag.

At Mine Mirth LLC, we cut through the financial noise to give you clear, actionable insights. The conversation between the Fed and the bond market is one we’ll continue to watch closely for you.

Disclaimer: This blog post is for informational and educational purposes only from Mine Mirth LLC. It is not personalized financial advice. Please consult with a qualified financial professional for advice tailored to your specific situation.